Microfinance is the provision of financial services to low-income clients or solidarity lending groups including consumers and the self-employed, who traditionally lack access to banking and related services.

More broadly, it is a movement whose object is "a world in which as many poor and near-poor households as possible have permanent access to an appropriate range of high quality financial services, including not just credit but also savings, insurance, and fund transfers." Those who promote microfinance generally believe that such access will help poor people out of poverty.

BOUNDARIES AND PRINCIPLES

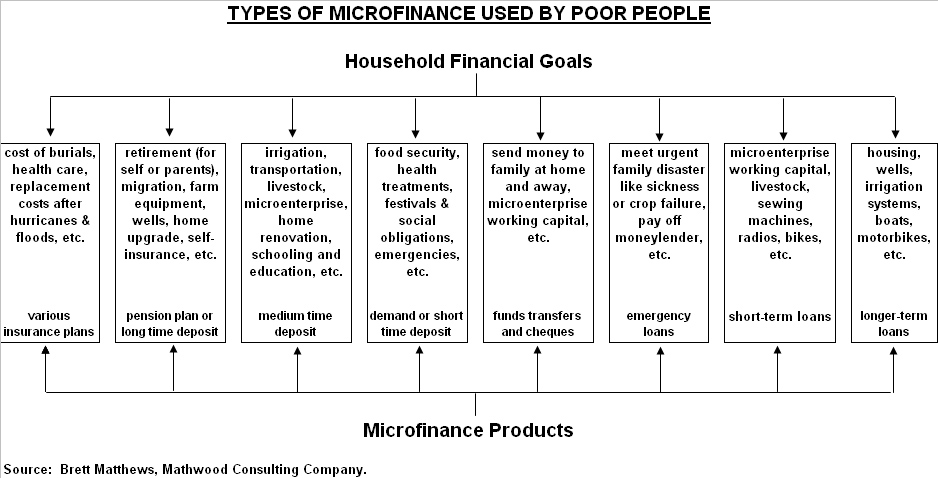

Poor people borrow from informal moneylenders and save with informal collectors. They receive loans and grants from charities. They buy insurance from state-owned companies. They receive funds transfers through formal or informal remittance networks. It is not easy to distinguish microfinance from similar activities. It could be claimed that a government that orders state banks to open deposit accounts for poor consumers, or a moneylender that engages in usury, or a charity that runs a heifer pool are engaged in microfinance.

CURRENT SCALE OF MICROFINANCE OPERATIONS

No systematic effort to map the distribution of microfinance has yet been undertaken. A useful recent benchmark was established by an analysis of 'alternative financial institutions' in the developing world in 2004. The authors counted approximately 665 million client accounts at over 3,000 institutions that are serving people who are poorer than those served by the commercial banks. Of these accounts, 120 million were with institutions normally understood to practice microfinance. Reflecting the diverse historical roots of the movement, however, they also included postal savings banks (318 million accounts), state agricultural and development banks (172 million accounts), financial cooperatives and credit unions (35 million accounts) and specialized rural banks (19 million accounts).

OTHER CRITICISMS

Most criticisms of microfinance have actually been criticisms of microcredit, delivered in the absence of other microfinance services such as savings, remittances, payments and insurance.

For example, there has been much criticism of the high interest rates charged to borrowers. The real average portfolio yield cited by the sample of 704 microfinance institutions that voluntarily submitted reports to the MicroBanking Bulletin in 2006 was 22.3% annually. However, annual rates charged to clients are higher, as they also include local inflation and the bad debt expenses of the microfinance institution.[38] Muhammad Yunus has recently made much of this point, and in his latest book argues that microfinance institutions that charge more than 15% above their long-term operating costs should face penalties.

Milford Bateman, the author of Why Doesn't Microfinance Work?, argues that microcredit offers only an "illusion of poverty reduction".

To read & know completely(78KB) click here

More broadly, it is a movement whose object is "a world in which as many poor and near-poor households as possible have permanent access to an appropriate range of high quality financial services, including not just credit but also savings, insurance, and fund transfers." Those who promote microfinance generally believe that such access will help poor people out of poverty.

BOUNDARIES AND PRINCIPLES

Poor people borrow from informal moneylenders and save with informal collectors. They receive loans and grants from charities. They buy insurance from state-owned companies. They receive funds transfers through formal or informal remittance networks. It is not easy to distinguish microfinance from similar activities. It could be claimed that a government that orders state banks to open deposit accounts for poor consumers, or a moneylender that engages in usury, or a charity that runs a heifer pool are engaged in microfinance.

CURRENT SCALE OF MICROFINANCE OPERATIONS

No systematic effort to map the distribution of microfinance has yet been undertaken. A useful recent benchmark was established by an analysis of 'alternative financial institutions' in the developing world in 2004. The authors counted approximately 665 million client accounts at over 3,000 institutions that are serving people who are poorer than those served by the commercial banks. Of these accounts, 120 million were with institutions normally understood to practice microfinance. Reflecting the diverse historical roots of the movement, however, they also included postal savings banks (318 million accounts), state agricultural and development banks (172 million accounts), financial cooperatives and credit unions (35 million accounts) and specialized rural banks (19 million accounts).

OTHER CRITICISMS

Most criticisms of microfinance have actually been criticisms of microcredit, delivered in the absence of other microfinance services such as savings, remittances, payments and insurance.

For example, there has been much criticism of the high interest rates charged to borrowers. The real average portfolio yield cited by the sample of 704 microfinance institutions that voluntarily submitted reports to the MicroBanking Bulletin in 2006 was 22.3% annually. However, annual rates charged to clients are higher, as they also include local inflation and the bad debt expenses of the microfinance institution.[38] Muhammad Yunus has recently made much of this point, and in his latest book argues that microfinance institutions that charge more than 15% above their long-term operating costs should face penalties.

Milford Bateman, the author of Why Doesn't Microfinance Work?, argues that microcredit offers only an "illusion of poverty reduction".

To read & know completely(78KB) click here

No comments:

Post a Comment